On September 22nd, nearly 700 venues lit up in red across the country to raise awareness of job losses among live event workers. As a matter of fact, all employment indicators in performing arts and entertainment industries once again fell in September.

Employment in Performing arts, spectator sports and related industries was 27% lower in September than a year ago at the same time. Moreover, labour force participation statistics suggest that workers are leaving the sector to find work elsewhere.

In order to provide a detailed picture of job losses in the arts, culture and heritage sub-sectors during the COVID-19 crisis, CAPACOA licenced access to custom employment statistics from Statistics Canada. These statistics are from the Labour Force Survey, a monthly survey of approximately 56,000 households. They provide an account of employment for full-time, part-time and occasional employees, as well as self-employed workers.

As of September, we are introducing a new table on labour force participation. Total labour force estimates provide a count of persons who were either employed or unemployed and available for work.

This month, we are also adding cultural industries sub-sectors to each data table. The focus of our analysis will however remain the live performance domain, which is contained within the performing arts, spectator sports and related industries sub-sector.

Key indicators for September 2020

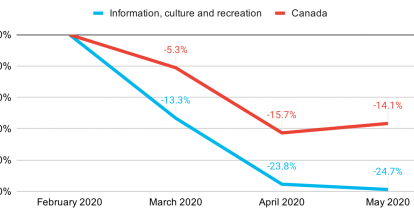

- Labour force participation held steady across most information, culture and recreation sub-sectors, except for one notable exception. Total labour force in performing arts, spectator sports and related industries [711] was 19.2% lower in September 2020 than at the same period last year. This means as many as 30,000 performing arts and entertainment workers were either not looking for work or they had left the sub-sector to find a job elsewhere in the Canadian economy.

- Employment in information and cultural industries [51] increased 4.2% in September. The increase is driven mainly by publishing industries [511] and other information services [519]. Total actual hours worked in information and cultural industries increased 18.5%. With the exception of motion picture and sound recording [512] and data processing, hosting and related services [518] employment and hours work are at or above pre-COVID levels.

- After modest increases in July and August, employment in the arts, entertainment and recreation sector [71] fell 10.6% in September. This decrease was most deeply felt in sub-sectors that had benefited from significant increases in previous months: heritage institutions [712] and amusement, gambling and recreation industries [713]. Total actual hours worked in the arts, entertainment and recreation sector fell by roughly the same proportion as employment: they went down 13.1%. They were 28.9% lower than a year ago for the same period.

- In spite of what Statistics Canada reports in The Daily, in proportion to its size, the arts, entertainment and recreation sector is the furthest away from recovery (see the note below).

Focus on live performance industries

- Performing arts, spectator sports and related industries [711] lost 3,000 more jobs in September (-2.7%). This brings employment back to the record low observed in April. Employment is now 27.0% lower than a year ago. In relative terms, this is the worst we’ve seen since the beginning of the crisis. In comparison, back in April employment was 24.8% below pre-COVID level.

- Total actual hours worked in performing arts, spectator sports and related industries [711] went down 2.4% in September. On average, employed persons worked 22.0 hours. Total and average hours worked nonetheless kept decreasing compared to pre-COVID levels (-43.6% and -22.5%, respectively).

- The labour force count is a particularly worrisome indicator. With 19.2% of the workforce gone in September 2020 compared to September 2019, the sub-sector runs the risk of facing a major shortage of skilled workers when live performance activities (finally) resume.

Which industry is the hardest hit?

In The Daily, Statistics Canada reports: “The accommodation and food services (-188,000) and retail trade (-146,000) industries remained furthest from full recovery” (adjusted for seasonality, compared to February 2020). This statement is incomplete.

In terms of the absolute number of jobs lost, the arts, entertainment and recreation sector is on par with retail trade (unadjusted for seasonality, compared to the same month the year before [see the technical notes below about seasonal adjustment]). In terms of the proportion of jobs lost, the arts, entertainment and recreation sector is the furthest away from full recovery:

- Retail trade: -3.3%

- Accommodation and food services: -15.2%

- Arts, entertainment and recreation: -16.5%

This fact is obscured in Statistics Canada’s analysis because its data tables aggregate a sector that has gained jobs (51 Information and cultural industries; +11.2%) with a sector that has lost jobs (71 Arts, entertainment and recreation; -16.5%).

Table 1 – Labour force estimates (x 1,000) by selected industry, Canada, unadjusted for seasonality

| Industry (with NAICS classification) | Labour force, Sept. 2020 (x 1,000) | c. previous month (x1,000) | c. previous month (%) | Sep. 2020 c. Sep. 2019 (x 1,000) | Sep. 2020 c. Sep. 2019 (%) |

|---|---|---|---|---|---|

| Total, all industries | 20264.6 | -286.7 | -1.4% | -3.7 | 0.0% |

| 51, 71 Information, culture and recreation 1 | 812.2 | -64 | -7.3% | 13.8 | 1.7% |

| 51 Information and cultural industries | 382 | 1.8 | 0.5% | 40.3 | 11.8% |

| 511 Publishing industries (except internet) | 71.6 | 5.5 | 8.3% | 8.7 | 13.8% |

| 512 Motion picture and sound recording industries | 86.6 | -4.5 | -4.9% | 0.5 | 0.6% |

| 515 Broadcasting (except internet) | 40.9 | 3.6 | 9.7% | -0.5 | -1.2% |

| 517 Telecommunications | 146.2 | -2.8 | -1.9% | 31.1 | 27.0% |

| 518 Data processing, hosting, and related services 2 | 6.7 | -0.7 | -9.5% | -3.3 | -33.0% |

| 519 Other information services | 30.1 | 0.8 | 2.7% | 3.7 | 14.0% |

| 71 Arts, entertainment and recreation | 430.2 | -65.8 | -13.3% | -26.5 | -5.8% |

| 711 Performing arts, spectator sports and related industries | 125.1 | -5.2 | -4.0% | -29.7 | -19.2% |

| 7111 Performing arts companies 2 | 27.4 | 3.9 | 16.6% | -19.8 | -41.9% |

| 7112 Spectator sports 2 | 5.9 | -3.3 | -35.9% | -11.8 | -66.7% |

| 7113 Promoters (presenters) of performing arts, sports and similar events 2 | 12.4 | -2.1 | -14.5% | 2.8 | 29.2% |

| 7114 Agents and managers for artists, athletes, entertainers and other public figures 3 | x | x | x | x | x |

| 7115 Independent artists, writers and performers | 77.5 | -4.4 | -5.4% | 1.3 | 1.7% |

| 712 Heritage institutions | 35.6 | -7.6 | -17.6% | 1.4 | 4.1% |

| 713 Amusement, gambling and recreation industries | 269.4 | -53.1 | -16.5% | 1.6 | 0.6% |

Table 2 – Employment estimates (x 1,000), by selected industries, Canada, unadjusted for seasonality

| Industry (with NAICS classification) | Employment, Sep. 2020 (x 1,000) | c. previous month (x1,000) | c. previous month (%) | Sep. 2020 c. Sep. 2019 (x 1,000) | Sep. 2020 c. Sep. 2019 (%) |

|---|---|---|---|---|---|

| Total, all industries | 18564.5 | 275 | 1.5% | -684.3 | -3.6% |

| 51, 71 Information, culture and recreation 1 | 727.5 | -28.3 | -3.7% | -34.8 | -4.6% |

| 51 Information and cultural industries | 365.7 | 14.8 | 4.2% | 36.8 | 11.2% |

| 511 Publishing industries (except internet) | 69.3 | 6.4 | 10.2% | 8.6 | 14.2% |

| 512 Motion picture and sound recording industries | 78.7 | 4.6 | 6.2% | -4.3 | -5.2% |

| 515 Broadcasting (except internet) | 40.9 | 3.6 | 9.7% | -0.5 | -1.2% |

| 517 Telecommunications | 142.2 | -3.2 | -2.2% | 32.4 | 29.5% |

| 518 Data processing, hosting, and related services 2 | 6.7 | -0.7 | -9.5% | -3.3 | -33.0% |

| 519 Other information services 2 | 28.5 | 3.1 | 12.2% | 2.3 | 8.8% |

| 71 Arts, entertainment and recreation | 361.8 | -43.1 | -10.6% | -71.6 | -16.5% |

| 711 Performing arts, spectator sports and related industries | 108.9 | -3 | -2.7% | -40.2 | -27.0% |

| 7111 Performing arts companies 2 | 19 | 1.5 | 8.6% | -26.6 | -58.3% |

| 7112 Spectator sports 3 | x | x | x | -11.9 | x |

| 7113 Promoters (presenters) of performing arts, sports and similar events 2 | 9.3 | -0.1 | -1.1% | 1.9 | 25.7% |

| 7114 Agents and managers for artists, athletes, entertainers and other public figures 3 | x | x | x | -2.5 | x |

| 7115 Independent artists, writers and performers | 75.2 | -1 | -1.3% | -1 | -1.3% |

| 712 Heritage institutions 2 | 32.3 | -6.7 | -17.2% | -0.3 | -0.9% |

| 713 Amusement, gambling and recreation industries | 220.5 | -33.5 | -13.2% | -31.2 | -12.4% |

Table 3 – Total actual hours worked estimates (x 1,000), by selected industries, Canada, unadjusted for seasonality

| Industry (with NAICS classification) | Total actual hours (x 1,000), Sep. 2020 | c. previous month (%) | Sep. 2020 c. Sep. 2019 (%) |

|---|---|---|---|

| Total, all industries | 607250.2 | 11.4% | -6.0% |

| 51, 71 Information, culture and recreation 1 | 21689.8 | 3.6% | -8.7% |

| 51 Information and cultural industries | 13094.8 | 18.5% | 12.1% |

| 511 Publishing industries (except internet) | 2490.1 | 19.4% | 17.3% |

| 512 Motion picture and sound recording industries | 2789.5 | 24.8% | -3.4% |

| 515 Broadcasting (except internet) | 1453.6 | 40.4% | 6.6% |

| 517 Telecommunications | 5300.5 | 7.6% | 27.2% |

| 518 Data processing, hosting, and related services 2 | 265.4 | 3.8% | -30.8% |

| 519 Other information services 2 | 795.8 | 55.9% | 5.3% |

| 71 Arts, entertainment and recreation | 8595 | -13.1% | -28.9% |

| 711 Performing arts, spectator sports and related industries | 2392.5 | -2.4% | -43.6% |

| 7111 Performing arts companies 3 | x | x | x |

| 7112 Spectator sports 3 | x | x | x |

| 7113 Promoters (presenters) of performing arts, sports and similar events 3 | x | x | x |

| 7114 Agents and managers for artists, athletes, entertainers and other public figures 3 | x | x | x |

| 7115 Independent artists, writers and performers | 1668.2 | 7.1% | -16.3% |

| 712 Heritage institutions 2 | 988.7 | -19.3% | -10.1% |

| 713 Amusement, gambling and recreation industries | 5213.8 | -16.1% | -22.7% |

Notes

- This series aggregates two distinct sectors. Statistics Canada aggregates culture industries in such a way in order to ensure data quality at small geographic levels. This aggregated series is included in order to enable some degree of comparisons with data tables published by Statistics Canada. The aggregation was performed by CAPACOA and no coefficient of variation for this series was provided by Statistics Canada. However, the aggregated data is presumed to be reliable because the coefficient of variation for each sector is very low.

- The sample for this series is small. Month-to-month variations in this series should be interpreted with caution.

- The sample for this series is very small. Data is unreliable and unsuited for release.

Additional notes about the Labour Force Survey

- “Labour force” estimates are the number of persons 15 years of age and over who, during the reference week, were employed or unemployed. “Unemployed” means persons who were without work, had looked for work in the past four weeks, and were available for work. Unemployed persons retain the NAICS industry classification of their previous job.

- “Employment” includes full-time, part-time and occasional employees, as well as self-employed workers who worked during the reference week, no matter how many hours. Certain sub-sectors that include a large proportion of self-employed workers, for example, independent artists may therefore not show a significant drop because those freelance workers may still have been considered “working”.

- “Total actual hours worked” is a good indicator of the impacts of COVID-related restrictions on the labour force, because it offers an account of both the number of employed workers and the hours they worked. It is a particularly relevant indicator for sub-sectors that include a lot of freelance and occasional workers (and who may be deemed as “employed” even if they only worked a few hours during the reference period).

- These statistics are not adjusted for seasonality (whereas many Statistics Canada tables are). Many culture industries are subject to significant seasonal variations. In order to have a fair estimation of employment change compared to pre-COVID level, it is therefore preferable to establish comparisons with the same period in 2019 rather than with February 2020.

- The “711 Performing arts, spectator sports and related industries” sub-sector is a larger industry grouping than the “Live Performance” domain used in the Culture Satellite Account, but it is a fair proxy that can be tracked over time. The 711 sub-sector involves activities that aren’t part of the live performance domain such as 7112 Spectator sports, as well as parts of 7113, 7114 and 7115. Definitions for each industry group are available in the North American Industry Classification System 2017. More details on the mapping between NAICS 711 and the live performance domain can be found in the Classification Guide for the Canadian Framework for Culture Statistics 2011.

- Equivalent employment statistics for other sectors of the Canadian economy can be found in Table 14-10-0022-01 Labour force characteristics by industry, monthly, unadjusted for seasonality.

More information

More statistics from the Labour Force Survey in The Daily

Employment in arts and culture industries, August 2020

Prepared by: Frédéric Julien, Director of Research and Development.

Pingback: APAC Response to the Government of Alberta’s 2021 Budget Consultation